Narrative: The Smart Home is Stuck

Each narrative page (like this) has a page describing and evaluating the narrative, followed by all the posts on the site tagged with that narrative. Scroll down beyond the introduction to see the posts.

Narrative: The Smart Home is Stuck (Jan 28, 2017)

Written: January 28, 2017

The smart home has been a hot topic for several years now, but appears to have cooled somewhat lately as standard bearer Nest has run into some trouble. Though some of that trouble can be ascribed to internal cultural tensions at Alphabet following the restructuring there, it’s actually symptomatic of broader problems facing the smart home market. The key issue is that the retail DIY model is only really suitable for certain early adopters, but it will take a services model to take the smart home into the mainstream.

Nest did well in the early going by selling a smarter thermostat to those who felt comfortable buying and installing their own device, with the wiring expertise (and risks) that entailed. In time, smoke and carbon monoxide detectors followed, along with the acquisition of Dropcam and its home cameras. But what seems to have happened since is that Nest has slowly maxed out the addressable markets for each of these products among early adopters, with minimal enhancements to the products and nothing entirely new for some time now. Other smart home vendors have targeted other segments, whether lighting, outlets, or smart appliances of one kind or another.

There are several fundamental challenges with this retail, DIY approach: it’s expensive up front, it often requires electrical and other expertise many don’t have, the resulting set of devices is often fragmented and hard to control, and network issues can often stop things from working at all or working with each other. That’s not a recipe for mainstream adoption. The solution to all this is a services model, where a single company works with a homeowner to identify needs, and then specs out, installs, and manages a system paid for through monthly fees rather than a big outlay at the beginning of the project. This model reduces cost and complexity and lays the responsibility for the whole thing at the feet of a single company with the power to manage all the elements of the system.

There are a number of companies out there pursuing this model, including AT&T (Digital Life), Comcast, Vivint, and the white label provider Alarm.com, which works with many alarm system companies. Each of these companies offers installation, a monthly fee model, and management through consoles and apps. The smarter of these are now taking this further and providing more intelligent management, with Vivint’s recent launch of its Sky assistant a great example of where this space can go next. This services model is typically centered on the alarm system market, because that’s an existing monthly subscription model people understand, and a smarter approach is often a significant upgrade to what people are used to. A handful of additional devices are usually installed at the same time, whether locks, lighting systems, or cameras.

None of this is to say that the services model will immediately lead to all homes being overhauled with smart gear – the services model works well for a handful of fairly superficial changes in the home – thermostats, locks, security systems and cameras – but wholesale changes to lighting and outlets require a much bigger investment and for relatively little payback. The best opportunity for the smart home over the long term is therefore new builds and major renovations, which will give current and prospective homeowners the opportunity to start from scratch with smart systems, rather than having to rip and replace systems that seem to be working fine.

We have a long way to go in the smart home market, but today’s retail DIY model isn’t going to get us there. The services model will get us further down the road to mainstreaming home automation, but even that will only scratch the surface. This is going to be a long slog, and the companies that do best will be those that embrace services, installation, management, and integrated systems, not those that sell piece parts at Best Buy.

Microsoft Adds Integration with Five Smart Home Vendors to Cortana (Oct 9, 2017)

I haven’t seen an official announcement around this, but Windows Central reports that Microsoft has quietly added support for four smart home vendors – Nest, SmartThings, Hue, Wink, and Insteon – to its Cortana virtual assistant. On the one hand, this is good timing with the Harmon Kardon speaker apparently getting ready for launch, but on the other it’s odd given the recent voice assistant partnership between Microsoft and Amazon, a big selling point of which was being able to control smart home gear through Alexa. In fairness, the latter still has much broader support for smart home ecosystems than Cortana, but Microsoft’s assistant now talks to several of the largest, and these plans must have been in the works for months now, certainly before the Alexa partnership was announced. At any rate, it’s going to be much simpler to control these devices directly through Cortana than through the awkward two-step process the Alexa partnership would require, and this is a good addition ahead of the launch of Cortana-based speakers.

via Windows Central

Samsung and ADT Partner for Self-Install SmartThings-Based Alarm Service (Oct 3, 2017)

Samsung and ADT have announced a partnership which will combine Samsung’s SmartThings home automation gear with the alarm company’s security system and optional monitoring service. Consumers will buy at retail and install the system themselves, while professional monitoring by ADT will be an optional extra. This is something of a theme in recent weeks, with Nest’s recent launch of a self-install security system (also with a partnership with an existing company for monitoring) and a separate announcement by smaller smart home company Ring. I continue to be skeptical about the broad appeal of self-installed smart home systems, but there clearly is a segment of the population that’s willing to self install and manage, and expanding into security makes sense for them. At the same time, most buyers are likely to continue to go with service-based approaches to both security systems and broader smart home gear.

via Samsung/ADT

★ Nest Introduces First New Hardware Categories in Years, Enters Security Market (Sep 20, 2017)

Nest held a press conference in San Francisco today and introduced three new products including its first really new product categories since its 2014 acquisition of Dropcam (this chart I put together a while ago presents the picture prior to today). The theme of the event was progress towards Nest’s ultimate goal – creating “a home that takes care of the people inside it and the world around it.” That mission combines Apple’s tendency to reinvent familiar products in ways that makes them vastly easier and more pleasant to use (unsurprising given the Nest founders’ Apple heritage) with more of an environmental message, largely tied to the smart thermostats. The first product announced today was a new outdoor version of the Nest Cam IQ indoor camera announced recently which added smarts including facial recognition to reduce false alarms among other things. The second was the Nest Hello, a smart doorbell very much along the lines of others already in the market but again with some clever technology borrowed from the camera line, and is the only product announced today that won’t be available until next year. The third was Nest’s big new category, home security, in the form of the Nest Secure system, which combines a hub and sensors to monitor movement inside a home as well as doors and windows.

{kind=link}

The Nest product line now feels a lot more comprehensive than it did a couple of years ago, with smart thermostats, smoke/CO detectors, and indoor cameras for inside the home, outdoor cameras and the doorbell for outside it, and a security system to keep it all secure, plus integrations with various third parties for lighting and other device categories. But it’s very much still an off-the-shelf, DIY, pay-upfront approach to the smart home, which continues to limit the addressable market to people willing to tinker, take risks, and self-manage with their home gear. When new CEO Marwan Fawaz came on board, I had thought he might lead the company through a transformation to more of a services company, which would put it much more in line with the telcos, cable companies, and others already offering that model and thereby reaching a much broader market. But there’s little sign of that yet – the only service component announced today is provided through a partnership with a third party monitoring company, and the prices for the new gear remain high: Nest Cam IQ outdoor is $349 for one, the starter pack for Nest Secure is $499 but only comes with two sensors, with most homes likely requiring several more, with pricing for Hello yet to be announced.

As such, Nest continues to largely target people with higher disposable incomes and a willingness to self-install and self-manage. My Nest thermostats frequently disconnect randomly from the strong WiFi signal in my home and suffer from other glitches, so unless Nest has improved things dramatically in these new products they’re likely to require quite a bit of management. It’s also worth noting that there continues to be minimal integration with the rest of Alphabet – I’d hope that some of the clever detection stuff has leant on Alphabet’s broader AI and machine learning capabilities, and Google Assistant integration is coming to the Nest Cam IQ devices in a software update. But Nest feels like it’s still being run very much at arm’s length from Google, for better or worse.

via Nest

Nest Unveils Cheaper, Slightly Less Capable Thermostat E (Aug 31, 2017)

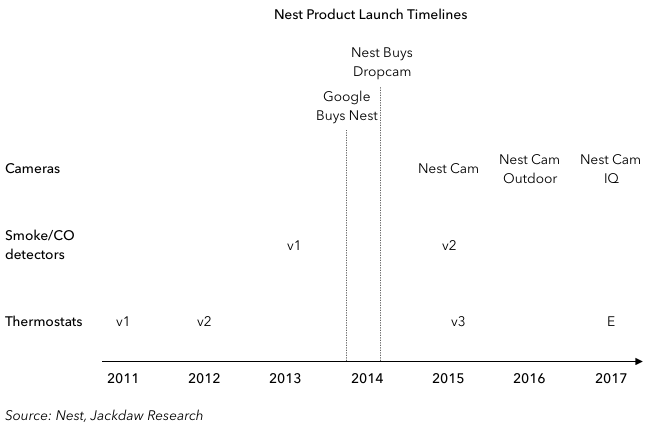

Nest unveiled its first new thermostat product in two years today in the form of the Thermostat E, a cheaper ($169 vs $249) and slightly less capable alternative to its core product line. The functionality is very similar, with only a slight reduction in compatibility with HVAC systems (Nest says 85% versus 95%) and one other minor missing feature relative to its core product. But the new thermostat is also redesigned, with a much lighter and arguably less distinctive look, apparently intended to blend in better to light colored walls and rooms rather than sticking out as an intentional piece of striking design like its first product in the category. Though the price of the original thermostat has certainly been a sticking point for some, especially those who need several units – the reality is that price is only one of many factors holding back the smart home. Far more important in many ways is the fact that most people find installing and managing these things intimidating and therefore managed services rather than DIY solutions are going to be the key for the vast majority of users, and Nest really isn’t doing anything in that direction. Meanwhile, Nest’s slow pace of new product introductions continues: it has three product lines, none of them newer than 2014, and its core thermostat and Protect products haven’t been updated in two years (see this image for an overview of its product launch history). The camera products have received most of the attention in the last couple of years, but there’s been no new organic product category from Nest since 2013. (See the Smart Home is Stuck narrative linked below for more context on all this)

via Nest

Samsung Announces Pricing and Availability for WiFi and Smart Home Hub (Jun 2, 2017)

Samsung announced its Connect Home mesh WiFi and smart home hub product alongside the new Galaxy S8 phones in March, but didn’t provide pricing or availability, something it’s now done. It will go on sale on Sunday at Best Buy and then become available more broadly in mid July, and will cost $170 for a single unit and three for $380, with a higher-throughput Pro version available for $250 per unit. The pricing is comparable with the many mesh WiFi solutions that have emerged in recent years, but the big difference is the SmartThings integration, which would normally involve a separate purchase. I’ll wait until reviews are available to judge it beyond that, but as I mentioned in the comment linked above back in March, it’s good to see Samsung finally starting to tie together its SmartThings and smartphone businesses, and I look forward to seeing whether that helps SmartThings get more traction in the market. The pure mesh WiFi space is certainly crowded enough already.

via Engadget

Nest Launches Smarter Security Camera for Inside Homes (May 31, 2017)

This content requires a subscription to Tech Narratives. Subscribe now by clicking on this link, or read more about subscriptions here.

Comcast Announces xFi WiFi Management Service for Broadband Customers (May 8, 2017)

This content requires a subscription to Tech Narratives. Subscribe now by clicking on this link, or read more about subscriptions here.

Ecobee Launches Thermostat with Alexa (May 3, 2017)

This content requires a subscription to Tech Narratives. Subscribe now by clicking on this link, or read more about subscriptions here.

★ Comcast Reports Slight TV Sub Growth, 1m Home Automation Customers (Apr 27, 2017)

Comcast reported Q1 2017 results this morning, and in keeping with past trends, the numbers were generally good. It saw another rise in TV subscribers as the cable companies continue to take share from the telcos, despite the overall trend of cord cutting, and it also saw strong growth in broadband subscribers, which now significantly outnumber its TV subs. Interestingly, it also began placing more emphasis on its home automation and security business this quarter, and reported that it has almost a million subscribers, or around 4% of its broadband base. The big theme that’s emerging from this quarter’s earnings reports from these providers is bundling – Comcast continues to see the percentage of customers taking more than one product rise over time (it’s now reached 71%), while AT&T suffered precisely because it can’t offer broadband/TV bundles to DirecTV customers. The wireless-TV bundles it can offer aren’t the ones consumers are looking for, which makes Comcast’s push into wireless somewhat questionable too. At NBCU, we’re seeing many of the same trends we’ve seen before too – subscriber numbers and viewing are down, but contractual rate increases with MVPDs are driving revenue growth anyway (of course those rate increases are rising costs on the cable side). Ad revenue was down in the cable networks business but up slightly in the broadcast business despite lower ratings because prices have been rising, though my analysis across the TV industry suggests the rate of price increases is slowing dramatically. Comcast continues to be a powerhouse across the categories where it competes (which also includes movies through Universal) but it’s facing some significant headwinds in the form of cord cutting, ratings declines, and rising content costs, which are going to take an increasing toll over the long term.

Note: you can see all my earnings posts or all Q1 2017 earnings posts specifically by clicking on the relevant tags below.

via Comcast